Money As Equity

We use debt as money, but is that really the best system?...

I’ve been thinking about the topic of this article for a while, but what really motivated me to sit down and write was a comment Matt Odell made on the Citadel Dispatch podcast recently. He said,

To me, that’s the cool part about Bitcoin, is that it’s this interoperable, permissionless, global network. And it’s almost like a shared equity, right? If you own Bitcoin the asset, it’s like we all share equity in this almost like a startup equity. And anything we do, and a lot of times it’s out of greed too. It’s not out of benevolence. You don’t have to be like a charitable person. But you know, if Strike benefits from something or Unchained Capital benefits from something, then Manchankura in Africa benefits from it as well at the same time, which is like a crazy concept. I feel like people just don’t really appreciate that.

When you start going down the “what is money?” rabbit hole, debt quickly comes into focus. You try to understand what it is, how it works, and why the world has so much of it and seemingly more by the second. Eventually you’ll discover that the “money” we use today is mostly just debt, created by banks when they make loans, and treated the same as the cash in your wallet. Until too many people try to withdraw their “money” from the bank, and the bank doesn’t have nearly enough cash to meet the withdrawals and collapses into insolvency. Which it always was, only no one realized who was swimming naked until the tide went out.

Equity is a related financial concept that doesn’t typically come up when studying money. The definition of the word as it’s used financially is something like “a risk interest or ownership right in property.” In simple terms, equity refers to ownership of something. For example, if you have a house that’s worth $500,000 and you have no mortgage or loans against the house, you have equity in the house of 100% of its value, or $500,000. If you have a mortgage of $250,000, you currently have 50% equity in the house, or you “own” half the value of the house.

It’s also often used to refer to shares issued by publicly traded companies. The shares represent a partial ownership of, or equity in, the company. If a company has issued 1,000 shares of stock and you own 10 shares, you have a 1% ownership of that company. That ownership give you certain privileges, such as dividends paid out from profits the company makes and potentially ownership of an increasingly valuable company, if it continues to be successful.

Money: Debt or Equity?

The current fractionally reserved fiat banking system primarily uses debt as money. There’s a small amount of base money, which consists of physical cash and a digital equivalent of cash called bank reserves, which are held in a ledger in banks’ accounts at the Federal Reserve and are used to settle transactions between banks. But this base money only makes up a small percentage of the total money supply. The bulk of the “money” consists of bank deposits, which are essentially IOUs created by banks when they issue loans under the fractional reserve system. When a bank makes a loan, they don’t actually give the borrower base money, for example a stack of physical cash, in most cases. Instead what they give is an liability entry in the bank’s balance sheet ledger that says “the bank owes the borrower this amount of dollars.” At the same time, on the asset side of the balance sheet they create another entry that says “the borrower owes the bank this amount of dollars” with details on how and when the loan must be repaid.

Then through the magic of banking, the borrower can transfer the numbers representing the amount the bank owes them to someone else, and now the bank owes that other person a certain number of dollars. And so on down the line. This can continue indefinitely, with people exchanging bank IOUs with each other in perpetuity, and no actual base money dollars needing to be exchanged. With help from a deliberate effort by banks to conceal the real nature of their activities, these credit/debt ledger entries function as, and for all practical purposes become, money. The only thing that can upset the apple cart is too many people trying to effectively exit the banking system at once, by trying to withdraw the money in their account. At that point reality sets in. The fact that the numbers in their account didn’t actually represent base money but rather just debt that the bank owes the depositor becomes obvious when the bank run reveals that the bank doesn’t have enough actual base money to settle its debt.

This system has a lot of serious problems, besides the fact that it’s fundamentally based on a lie. For one, all the bank deposits are created by making loans, which means they’re all debt, which means they all have to be paid back with interest. That’s a problem for two reasons. One, paying back the debt destroys money, which artificially disrupts the economy by distorting prices as the amount of money in the economy rises and falls arbitrarily depending on new loan issuance versus debt repayment. Two, when the loan is made, only the amount of the principle is created in bank deposits. The interest isn’t. That means new loans have to be made to pay the interest on the existing loans. That basically guarantees that the amount of debt in the economy will continue to rise indefinitely, because the only way it could go down is for the banking system as it currently exists to collapse, or to be “bailed out” with massive injections of newly created base money to offset loans that can’t be paid back. That, coincidentally, is what Quantitative Easing is; an injection of newly created base money to provide liquidity to pay back debt without having to issue new debt to do it.

Now let’s think for a minute about equity and how it might compare and contrast with the current system in relation to money.

To begin with, I understand money as a ledger of deferred consumption. If you haven’t heard that concept before, it would probably be helpful to familiarize yourself with my thought process laid out here.

Money Is Not Wealth

Of all the common misconceptions about money, this is the deepest and most pervasive. It taps into the very psychology that makes money the most powerful tool in the world. Money works in large part because, for most practical purposes, you can assume that money and wealth are the same thing and be very successful in life.

Deferred consumption is what makes capital formation and civilization possible. People work to create things that they don’t immediately consume, and those new tools and processes make it easier to create more things in the future with less effort, which raises the productivity of the economy (getting more output for less input) and makes society as a whole wealthier. Those new tools and processes can then be used to more efficiently create other tools and processes, which increases productivity even further, and the whole thing compounds on itself in an exponential curve of increasing productivity and increasing wealth. But it all starts with and relies on someone somewhere putting in effort now, to create something they won’t benefit from until later.

Planting a seed is a perfect example. When you have a bushel of wheat, you have two choices. You can consume it now. That’s immediately satisfying and keeps you fed for say a month. Or you can plant it. That’s hard work, and you also have to defer consumption of the wheat. You can’t eat it now, you have to satisfy your hunger some other way. It also takes work throughout the year to cultivate and care for the wheat crop, time you could have spent doing something more fun, if you had just consumed the wheat directly instead of planting it. The flip side is, at harvest time, you might harvest 50 bushels of wheat from the 1 bushel you didn’t eat 6 months ago. That 50 bushels could now feed you for 4 years, and you can sell 30 bushels, keep 12 for your own use over the next year, and plant 8 for harvest next year. Then in a year you might harvest 400 bushels, etc. You can see how a little bit of deferred consumption today can lead to a lot of reward in the future. There’s even a term for being short-sighted and sacrificing future rewards for present gratification, “eating the seed corn,” which comes directly from this farming wisdom.

The same principle applies to business equity. When you start a business, you invest in some way into building something that isn’t immediately rewarding, but that you expect will yield more production in the future than your initial investment. You might invest your own time and effort, resources that you’ve gathered, money, or any number of other forms of value. The same applies to a public company that issues equity as shares of stock. Anyone can invest in the company by purchasing shares, which gives them a partial ownership of the company and its future growth and production. All those forms of investment, to acquire equity, are different forms of deferred consumption. You have to give up something you could have now, for something you hope to have in the future. You could spend the time now curled up in bed binge-watching Netflix. You could spend your effort strolling down the boardwalk eating an ice cream cone. You could spend your money on that pricey designer bag that all your girlfriends will be jealous of. All those things would be immediately gratifying. But they all have a long-term cost.

What happens when you defer consumption instead, and acquire equity? If things go the way you hoped and planned, and the company you founded or invested in is successful, it will eventually produce more than the initial consumption that you deferred. Your equity will become more valuable with time. Why? Because like we pointed out, deferred consumption and capital formation increases efficiency, which leads to compounding returns in productivity and value.

If the company is extremely successful and you defer your consumption long enough, those returns can be very large. For example, if you had invested $1,000 in Amazon in 2007, that equity today, 17 years later, would have returned over $80,000. The first iPhone was released in 2007 for $500. So you could have bought two iPhones instead of making that initial investment in Amazon. But if you deferred that consumption instead, even though the price of the iPhone has doubled by 2024, you could still buy eighty new iPhones with the equity from that initial investment instead of two, or a 40x return in “iPhone inflation adjusted” terms.

Now let’s make a mental leap and compare equity in a business with money. We’ve defined money as a ledger of deferred consumption. You could define business equity as a ledger of consumption deferred to establish ownership of a business instead. You have the stock, the equity in the company, to represent that you invested your time, effort, resources or money into building a business rather than consuming it on something for your immediate gratification. These definitions seem very similar, almost synonymous. We could also consider the economy as a whole to be very similar to a business. As consumption is deferred, more capital is created in the economy, it becomes more efficient and productive, more outputs are created with fewer inputs, and the economy as a whole grows in value.

Business equity represents ownership in a company, both in the current value of that company, and in its future productivity and value. Why? Because the future productivity and value wouldn’t exist if it weren’t for the deferred consumption of the initial investment. If Jeff Bezos hadn’t started Amazon, and investors hadn’t provided the money by buying shares to enable the company to grow the way it did, all the productivity and value of Amazon today wouldn’t exist. That’s why it’s fair for the person who only invested $1,000 in 2007 to gain a return of 40x that investment today.

So if business equity represents ownership of a company earned by deferred consumption, what does the deferred consumption of money itself grant ownership of? Well, money can be exchanged for any good or service available on the market, throughout the entire economy. In my opinion, money should represent ownership of the future productivity and value of the economy as a whole. Money should be equity in civilization itself. The future productivity and value of the economy depends on the deferred consumption of today, just like the future productivity and value of a company depends on the deferred consumption of its initial founders and investors.

Slices of Pie

There’s an issue that needs to be addressed here, one that the savvy investor will have noticed already. Equity in a growing and successful company becomes more valuable over time. Yet even though the economy as a whole is becoming more productive and more valuable, money as we know it today becomes less valuable over time. The $1,000 Amazon equity went from being worth two iPhones, to being worth eighty iPhones. Over the same time period, the $1,000 itself went from being worth two iPhones to being worth one iPhone. What gives?

To understand, we have to look at the differences between how equity is created and how money is created.

The most simple example is a company that’s owned by a single individual. They hold 100% of the equity. You could call that one share. Think of the company like a pie, but the pie hasn’t been cut, so there’s only one “slice.” Over time, if the company is successful, the company “pie” grows larger. But as it grows, it doesn’t get cut into more slices, the one “slice” just gets bigger and bigger. So the one “share” of equity the owner holds is still one share, it’s just a bigger and more valuable share.

Public companies generally function similarly. They start out “going public” by issuing shares. Each share is like a small slice of the company “pie.” Say the company issues 1,000 shares, each share represents a slice of pie 1/1,000th the size of the whole company pie. If the company grows, it won’t commonly issue more shares, although that can happen in certain situations. Instead, the shares will continue to represent 1/1,000th of the company, it will just be 1/1,000 of a bigger and bigger “pie” as time goes on. If the company doubles in productivity and value, each share will be twice as valuable, while still only being one share.

That doesn’t have to be the case. The company can, and sometimes does, issue more shares of stock. The reason this isn’t commonly done, though, is that it’s usually bad for the holders of the stock. If the company issues another 1,000 shares, there are now 2,000 pieces of ownership of the company. The company is no bigger, it’s just divided into more pieces. It’s like cutting each slice of pie in half. You don’t have more pie, you just have more pieces of pie. And as someone who already had a piece of pie, your piece suddenly got cut in half. Of course you probably won’t be too happy about that situation. In effect, the value of the deferred consumption of your initial investment is being taken away from you and given to someone who didn’t defer consumption and therefore didn’t contribute to the success the company has already experienced.

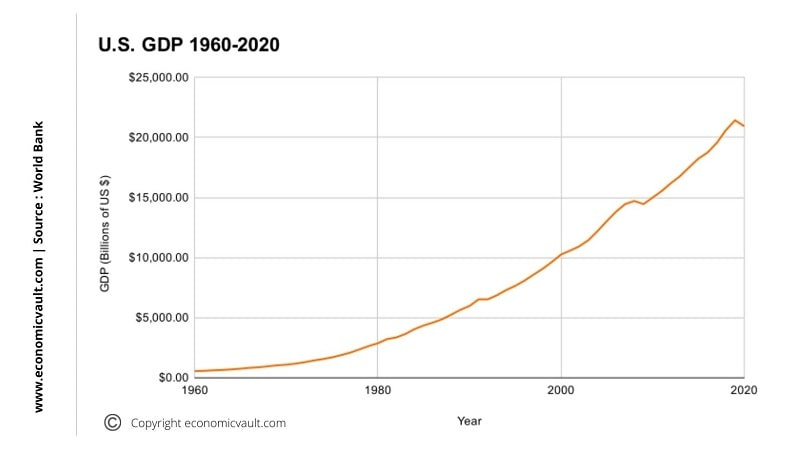

Contrast that to how money is created. If you compare the chart of money supply below with the chart of GDP, you'll see they both go up over time.

GDP is an (admittedly flawed) measure of the goods and services produced by an economy each year. It's similar to a company's revenue. As a company or economy grows and becomes more productive and valuable, the revenue or GDP rises. The thing about the economy though, is that money, the “shares” of an economy representing the deferred consumption that enables it to grow, is constantly being created by banks making new loans. So as the economy grows, the number of “slices” of the economy grows even faster. When the number of “slices” of an economy grow faster than the economy itself, the “size” or value of each slice falls over time. This is what we call inflation. It takes more “slices” of the economy to buy something than it did in the past, even though the economy is more efficient at producing that good or service than it was in the past.

You can imagine how it might look if a company managed its equity the way the banks manage our money. Each year, as the company grew, the board of directors would issue enough new shares of stock to make sure the value of each share fell that year. They could take the approach the US banking system takes and “target 2% inflation,” in other words try to make the share value fall 2% every year. So if the productivity and value of the company increased by 10%, the board would issue 12% more shares to dilute the existing shareholders by the full amount of the increased value of the company, plus an additional 2%. This would help ensure the share price fell 2% every year. The new shares would be distributed to existing shareholders arbitrarily by decision of the board, with a big chunk going to the board members themselves. This would be highly profitable for the board, leaving them with a larger slice of company equity every year, while being very damaging to all the other shareholders.

In fact, one might wonder why an investor would ever hold equity in a company, when the company's stated policy was to reduce the value of that equity by 2% every year. The answer is, nobody would. It would be idiotic.

Then one might wonder why anyone would hold money, “shares” of an economy, when the stated policy of the banks managing the issuance of that money is to reduce the value of each dollar by 2% every year. The answer to that is just as simple: they have to.

Nobody has to buy stock issued by a particular company in order to survive day to day. But it’s impossible to survive day to day in the modern US economy without using the money issued by the US banking system. You get paid in dollars for your work, and get charged in dollars for every item you buy. You need at least a certain amount of dollars just to live day to day. Of course those who understand the financial system make every effort to hold as few dollars as possible, and to invest the excess as soon as possible into some asset that will hold its value over time. Of course that doesn’t actually get rid of the dollar, just transfers it to someone else. Then the new holder of the dollar has to quickly exchange it with someone else for a better asset, and so on in an endless repeating loop. No matter how many people invest in assets, the full quantity of dollars in existence is always held by someone, and those people are continually being diluted by the issuance of new dollars by banks creating bank deposits when they make loans.

Implications

If what I’m proposing is correct, there would be massive implications in changing the way money works in the economy from the current credit/debt issuance controlled by banks, to a system that functions more like equity issued by a responsible and profitable company. Getting into the details of those implications in various specific areas will take many more articles, but I just want to mention a few to get your mind running, then circle all the way back to where we started.

Imagine if the money every person earned went up in value as the economy grew. It would be like owning equity in the broadest possible index of businesses, better even than owning an S&P 500 ETF or mutual fund. And it would take no effort. There would be no need to open a brokerage account, decide what companies or funds to invest in, and pay commissions and fees to the brokerage for the privilege. There would be no need for a 401k. All that would be needed is to work at the job you’re best at, consume less than you produce, and save the difference. The economic growth created by increased productivity would automatically accrue equally across the population to those who were best at being productive and deferring consumption. Working hard, being frugal, and saving for the future would automatically be rewarded. All the incentives would be realigned to benefit those who contribute most to capital formation and future economic prosperity.

It would be much easier for those with low income to get ahead financially. Any amount they manage to save, no matter how small, would increase in value over time. Contrast that with the current system where a small amount of savings continually becomes worth less over time, encouraging people to consume more than they need in the moment since their small savings will shrink to insignificance quickly.

You can easily think of lots of other changes that would happen as a result of using money that functions more like equity than our current system does.

But to tie all this back to the quote at the beginning, I think what Matt is seeing and feeling is the beginnings of a more equity-like monetary system. I think the properties of Bitcoin, specifically its predictable and limited supply issuance, make it behave like equity in a well-managed, productive company. That “company” just happens to be the global and permissionless group of every person who chooses to save and transact in Bitcoin instead of the current credit/debt money. And the fact that even self-serving actions toward productive goals end up benefitting every member of the network is exactly what we’d expect in a truly capitalist economic system. Whenever someone works to grow the “pie” in order to make their slice bigger, the fact that the pie is growing means everyone else’s slice is growing as well. And that’s a beautiful thing.

I’m excited to see how this theory plays out over time, because from my point of view, the potential of moving to a more equity-like monetary system is both massive and extremely optimistic.

Great article F0xr, i found my way here from your Nostr post. This is very easy to read and a resource for people starting to find their way down the "what is money" rabbit hole. Keep writing..

If only working hard and being frugal was automatically rewarding🤭 I like your article it's simple enough for this carpenter to follow. And I will follow for more content. Eating the seed corn is a saying that I will try to incorporate into conversations in the future..